Finances are the foundation...

You have heard it said that your business' finances are the foundation of your program. Sound financial planning can and will determine the success of any business. Good financial management and planning helps you efficiently use the limited resources you have to provide a quality program for the families you serve. The budget is a plan of the amount of income and expenses for a set period of time in the future. Budgets project income and expenses in the future. Budgets also can be used to:

* set limits on your spending

* set financial goals for your program

* help make financial decisions

A good budget is realistic. Even though it looks good to compile an overly optimistic budget, it doesn’t help you make good decisions.

Budgets cover a set period of time; often monthly, quarterly or yearly. However, some budgets such as a start-up budget will be for a period of time that will cover a specific activity. The budget starts when the activity starts and ends when the activity ends.

Operating Budget (Annual Budget)

The Operating Budget is a projection of your income and expenses for the day-to-day operation of your program. It includes all of your income and expenses. To develop an Operating Budget, it helps to look at the actual income and expenses from past years. This is only possible if the program has been operating for a number of years. If you are using historical data you should collect the last three to five years of financial statements such as budgets, actual expenses and/or tax forms.

* set limits on your spending

* set financial goals for your program

* help make financial decisions

A good budget is realistic. Even though it looks good to compile an overly optimistic budget, it doesn’t help you make good decisions.

Budgets cover a set period of time; often monthly, quarterly or yearly. However, some budgets such as a start-up budget will be for a period of time that will cover a specific activity. The budget starts when the activity starts and ends when the activity ends.

Operating Budget (Annual Budget)

The Operating Budget is a projection of your income and expenses for the day-to-day operation of your program. It includes all of your income and expenses. To develop an Operating Budget, it helps to look at the actual income and expenses from past years. This is only possible if the program has been operating for a number of years. If you are using historical data you should collect the last three to five years of financial statements such as budgets, actual expenses and/or tax forms.

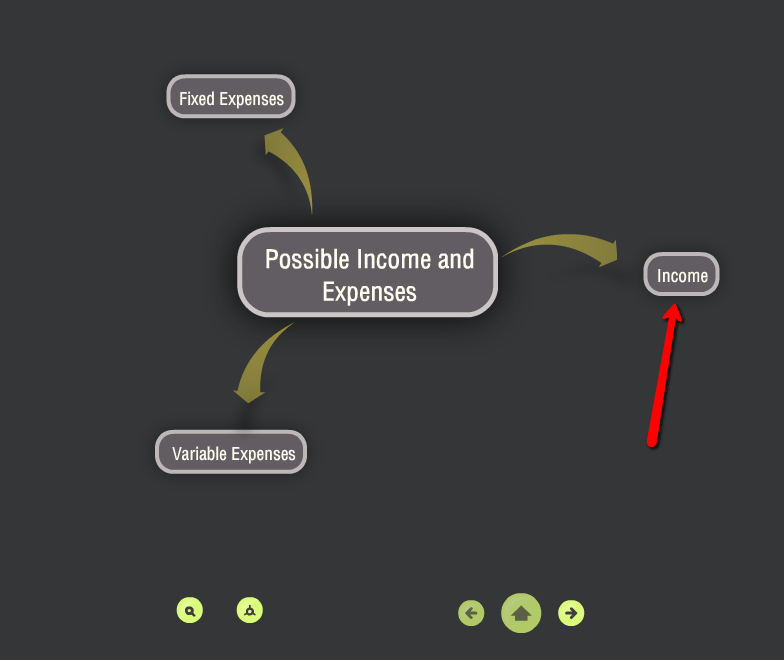

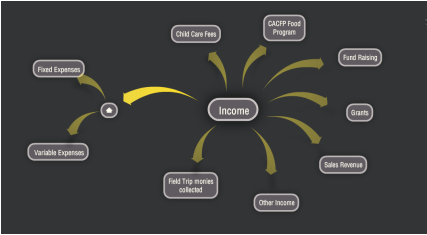

Possible Income and Expenses

Preparing a budget helps you define where you expect the money to come from and how you expect to spend it. It gives you a picture of whether your projected income will meet your expected expenses.

Have you ever wondered what Income and Expenses you should include in your budget? Look no further... click on this link for an interactive tool that will illustrate line items:

http://www.spicynodes.org/a/52ff665c50450d9ef86b69bdcb53a62d

When the link opens (it may take a minute) you will see a wide range of possible income sources and expenses in any child care program. However, if you are having difficulties opening the link, you can view the contents here:

Have you ever wondered what Income and Expenses you should include in your budget? Look no further... click on this link for an interactive tool that will illustrate line items:

http://www.spicynodes.org/a/52ff665c50450d9ef86b69bdcb53a62d

When the link opens (it may take a minute) you will see a wide range of possible income sources and expenses in any child care program. However, if you are having difficulties opening the link, you can view the contents here:

| list_of_income_and_expense_categories.docx |

Now, simply click on any of the gray buttons and see what pops up! Or click on the picture of the house to go back to the beginning.

Which of these incomes and expenses apply to you and your program? It's ok that they all don't, but some of these might spark a new thought on some potential income or expenses you hadn't thought of!

Budgeting Tip (from First Children's Finance)

When estimating income, research shows that enrollment for start-up centers is typically 50-65% of licensed capacity. Even when fully enrolled, a center will rarely reach and maintain 100% capacity. A realistic figure is 85-95% licensed capacity.

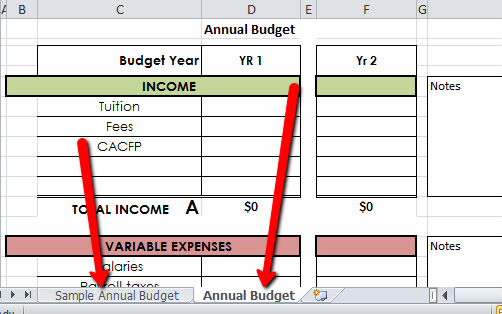

Line Item Budget

When the spreadsheet opens, you will notice at the bottom there are 2 tabs: Sample Annual Budget and Annual Budget. The Sample Budget offers some directions on how to fill out the Annual Budget. You might also notice that this Annual Budget has 2 years on it. Year 1 is for the current year and Year 2 is for the following year. This allows you to do some simple comparisons of budgets.

You will also notice that some categories have been filled in for you. These are suggestions based on common line items relevant to many programs. There are additional spaces available to customize this document. On the Annual Budget page, the Total Income will calculate for you as you enter amounts next to each category.

You will also notice that some categories have been filled in for you. These are suggestions based on common line items relevant to many programs. There are additional spaces available to customize this document. On the Annual Budget page, the Total Income will calculate for you as you enter amounts next to each category.

Next, under the Income section is the Expense section. This portion of the spreadsheet is broken down by Variable expenses and Fixed expenses.

Let's take some time to look at the difference between Variable and Fixed expenses and why it's important to separate them on your budget.

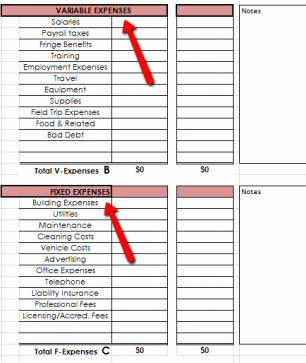

Variable Expenses

Variable expenses are costs that are based upon the number of children enrolled. When a new child enrolls in your program the amount of money you spend on variable expenses will increase. When a child withdraws from your program the amount you spend on variable expenses will decrease. Over 50% of most programs' expenses are spent on salaries and salary-related costs. If these expenses are not managed, your program's financial health can be in jeopardy. However, cutting these costs by under staffing, paying low wages or eliminating benefits can also cause problems. Salaries are considered variable expenses because the total amount spent will change when the number of staff changes, which results when the number of children change. Salary-related expenses include payroll taxes (Social Security and Medicare Taxes, State and Federal Unemployment Tax, and Worker's Compensation Insurance), as well as fringe benefits like health insurance or paid sick leave.

Training and Travel expenses also fall under the variable category because these costs tend to fluctuate from year to year depending on program goals. For example, this year you may choose to attend a national conference, but you may not plan on doing that every year. Or you may decide to send all your teachers to a state conference as money allows, but this may not occur every year.

Another example of a variable expense is program equipment and supplies. These refer to those consumable supplies that must be replenished every so often and are affected by the number of children enrolled. Materials such as puzzles, books, paint, construction paper, etc. Equipment expenses are those items used by teachers and children such as furniture. Some furniture or other big ticket times may be depreciated over time. Consult your accountant to determine which purchases you may be required to depreciate.

Field trip expenses are only incurred if you do not charge parents the full cost of the field trip. You must take into consideration admission fees, transportation, and any additional staffing that may be needed.

Food-related costs fluctuate dramatically depending on the number of children enrolled. These costs include food, plates, cups, silverware, pans, kitchen equipment, and other related costs.

Finally, bad debt expenses are incurred for collecting money from parents. These costs would include collection fees, attorney's fees, court fees and other related costs.

Training and Travel expenses also fall under the variable category because these costs tend to fluctuate from year to year depending on program goals. For example, this year you may choose to attend a national conference, but you may not plan on doing that every year. Or you may decide to send all your teachers to a state conference as money allows, but this may not occur every year.

Another example of a variable expense is program equipment and supplies. These refer to those consumable supplies that must be replenished every so often and are affected by the number of children enrolled. Materials such as puzzles, books, paint, construction paper, etc. Equipment expenses are those items used by teachers and children such as furniture. Some furniture or other big ticket times may be depreciated over time. Consult your accountant to determine which purchases you may be required to depreciate.

Field trip expenses are only incurred if you do not charge parents the full cost of the field trip. You must take into consideration admission fees, transportation, and any additional staffing that may be needed.

Food-related costs fluctuate dramatically depending on the number of children enrolled. These costs include food, plates, cups, silverware, pans, kitchen equipment, and other related costs.

Finally, bad debt expenses are incurred for collecting money from parents. These costs would include collection fees, attorney's fees, court fees and other related costs.

Fixed Expenses

Unlike variable expenses, fixed expenses do NOT change when staffing or attendance changes. An increase in children does not lead to an increase in fixed costs.

There are several expenses that are considered building expenses. They include: rent/lease/mortgage, mortgage interest, building depreciation, property taxes, and building insurance. Some of these expense items are used when the program owns the building like mortgage interest, building depreciation and capital improvements. Others are used when you lease the building like rent and leasehold improvements. The amount of the occupancy costs often depends upon the size of your facility, the larger the building the higher the cost. Occupancy costs are considered fixed because they do not change when your enrollment changes.

Other fixed costs may include Advertising, Office Expense, Telephone Costs, Insurance and Professional Fees like a lawyer or accountant.

There are several expenses that are considered building expenses. They include: rent/lease/mortgage, mortgage interest, building depreciation, property taxes, and building insurance. Some of these expense items are used when the program owns the building like mortgage interest, building depreciation and capital improvements. Others are used when you lease the building like rent and leasehold improvements. The amount of the occupancy costs often depends upon the size of your facility, the larger the building the higher the cost. Occupancy costs are considered fixed because they do not change when your enrollment changes.

Other fixed costs may include Advertising, Office Expense, Telephone Costs, Insurance and Professional Fees like a lawyer or accountant.

Click on the "Line Item Budget" document below to open. Save to your computer, and then consider printing. This document does not open in a new window, so you will have to click on the 'back arrow' in the upper left corner of your computer screen to go back to the tutorial. You may have to 'enable editing' once this document opens, depending on the Office version you have.

| line_item_budget.xls |

Questions to consider...

Consider how you would answer these questions - use your answers to develop and implement financial practices and policies that will help support the financial health of your program.

1. Does our program have a current annual budget?

2. How detailed is the budget?

3. Do we have line items?

4. Does our budget project a profit or a loss? What makes that true?

1. Does our program have a current annual budget?

2. How detailed is the budget?

3. Do we have line items?

4. Does our budget project a profit or a loss? What makes that true?

YoungStar Requirements

Under the Business and Professional Practices section of YoungStar, group centers are required to have an ongoing annual line-item budget for 3, 4 and 5 Stars.

The line-item budget must include projected income and expenses for the current year divided into line-items. This is to be a 12-month budget but does not necessarily need to follow the calendar year (January to December). Programs may choose to follow the state or federal fiscal calendar (July to June) or some other time period. The requirement is to show 12 months as a whole or it and can be broken down monthly or quarterly, depending on the program's preference.

One line-item should include funding for at least one item in the program's Quality Improvement Plan (QIP): this may be a line-item by itself or may be an item within a line-item. For example, a program may have WMELS training in their QIP and that may be shown within a line-item for "Training" or may be named "QIP" explicitly.

The working budget in this tutorial is an annual line-item budget and does not explicitly offer a separate line for QIP. Feel free to include that line-item if that meets the needs and direction of your program. Although the line-item budget in this tutorial is designed as a yearly budget, you may choose to use it quarterly (every 3 months) or monthly; just be sure to indicate on the budget what timeframe the budget covers.

The line-item budget must include projected income and expenses for the current year divided into line-items. This is to be a 12-month budget but does not necessarily need to follow the calendar year (January to December). Programs may choose to follow the state or federal fiscal calendar (July to June) or some other time period. The requirement is to show 12 months as a whole or it and can be broken down monthly or quarterly, depending on the program's preference.

One line-item should include funding for at least one item in the program's Quality Improvement Plan (QIP): this may be a line-item by itself or may be an item within a line-item. For example, a program may have WMELS training in their QIP and that may be shown within a line-item for "Training" or may be named "QIP" explicitly.

The working budget in this tutorial is an annual line-item budget and does not explicitly offer a separate line for QIP. Feel free to include that line-item if that meets the needs and direction of your program. Although the line-item budget in this tutorial is designed as a yearly budget, you may choose to use it quarterly (every 3 months) or monthly; just be sure to indicate on the budget what timeframe the budget covers.

Disclaimer: Materials and links provided by WECA on this tutorial do not constitute legal, accounting, tax or finance advice. Participants seeking professional business advice about specific aspects of their program should consult a professional such as a lawyer, accountant, etc.