Family Child Care Providers work hard for their business. Sound financial planning helps make sure that their businesses work hard to support family child care providers. Sound financial planning is the process of implementing policies and practices which help ensure timely payments, an adequate cash flow and allows the provider to have a clear vision of the financial health of the business.

Budget Review

You've done the difficult, complicated part! Now comes the simple part...analyzing the numbers!

The Budget Review process allows you to think about whether the costs that you are incurring really help you to accomplish your mission and vision.

Are you using your money to help you accomplish your most important tasks? The process also helps you realize you have expenses that don't seem apparent at first glance. So the budget process from beginning to end helps you to better understand your program's total financial picture.

Take the necessary time to adequately review your financial statements. Compare your budget, which is your estimated income and expenses, to your actual income and expenses. Look for trends, both good and bad, that might affect your program's quest for high quality. Is your income growing from year to year or has it been declining? Are you spending more money on one line item than you thought? Why do you think that is? What can you do about it? These are all questions you can answer once you've taken the time to review your financial statements.

The Budget Review process allows you to think about whether the costs that you are incurring really help you to accomplish your mission and vision.

Are you using your money to help you accomplish your most important tasks? The process also helps you realize you have expenses that don't seem apparent at first glance. So the budget process from beginning to end helps you to better understand your program's total financial picture.

Take the necessary time to adequately review your financial statements. Compare your budget, which is your estimated income and expenses, to your actual income and expenses. Look for trends, both good and bad, that might affect your program's quest for high quality. Is your income growing from year to year or has it been declining? Are you spending more money on one line item than you thought? Why do you think that is? What can you do about it? These are all questions you can answer once you've taken the time to review your financial statements.

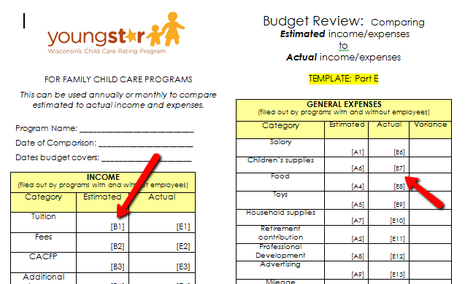

Completing your Budget Review worksheet will offer you great insight into when your program is bringing in more money than expected or when your program might be spending more money than expected. This is a nice snap-shot to see where your budgeted amounts are not matching your actual amounts after the year is done.

Variance

As part of your Budget Review, you will want to examine closely the differences between the actual income and expense with your Annual Budgeted income and expenses for each line item. For each category or line item that you were significantly off, is there a reason that helps explain the difference? In some cases, there may have been a specific cause for the large difference. (Example: a child damaged a significant piece of furniture and it had to be replaced, or your enrollment was significantly under or over‐budgeted.) For each line item, look at what you thought you would spend (budgeted/estimated) and what you actually spent. Decide which number seems like a more accurate picture for the next year, given what you know about your situation. If you are going to have a significant change that you are aware of (example: expanding licensing capacity, changing policies regarding full time or part time care, hiring an assistant), make sure to take that into consideration.

An idea would be to take notes to remind yourself why you are reviewing the figures you are for your budget. This may be called a budget justification. It helps to see how the figures were arrived at. For example, if my annual tuition line item is $37,500, I may want to make a note of the math used to figure that [$625 x 5 kids x 12 months] to help remind me. Then at the end of the year if my tuition is actually $41,500, a review of the justification and math equation would help me realize it was off because I actually ended up having a 6th child to care for during the year for 6 months. This resulted in an additional income tuition of $3750.00 [1 child x 6 months of care = 6; 6 x $625.00 for monthly tuition = $3750.00]. The actual tuition of $41,500 was increased by $3750 from the original of $37,500.

Variance

As part of your Budget Review, you will want to examine closely the differences between the actual income and expense with your Annual Budgeted income and expenses for each line item. For each category or line item that you were significantly off, is there a reason that helps explain the difference? In some cases, there may have been a specific cause for the large difference. (Example: a child damaged a significant piece of furniture and it had to be replaced, or your enrollment was significantly under or over‐budgeted.) For each line item, look at what you thought you would spend (budgeted/estimated) and what you actually spent. Decide which number seems like a more accurate picture for the next year, given what you know about your situation. If you are going to have a significant change that you are aware of (example: expanding licensing capacity, changing policies regarding full time or part time care, hiring an assistant), make sure to take that into consideration.

An idea would be to take notes to remind yourself why you are reviewing the figures you are for your budget. This may be called a budget justification. It helps to see how the figures were arrived at. For example, if my annual tuition line item is $37,500, I may want to make a note of the math used to figure that [$625 x 5 kids x 12 months] to help remind me. Then at the end of the year if my tuition is actually $41,500, a review of the justification and math equation would help me realize it was off because I actually ended up having a 6th child to care for during the year for 6 months. This resulted in an additional income tuition of $3750.00 [1 child x 6 months of care = 6; 6 x $625.00 for monthly tuition = $3750.00]. The actual tuition of $41,500 was increased by $3750 from the original of $37,500.

Click on the "Budget Review" documents below to open. Save to your computer, then consider printing the 'template'. This document does not open in a new window, so you will have to click on the 'back arrow' in the upper left corner of your computer screen to go back to the tutorial. You may have to 'enable editing' once this document opens, depending on the Office version you have.

|

| ||||

Questions to consider...

Consider how you would answer these questions -- use your answers to develop and implement financial practices and policies that will help support the financial health of your business.

1. How often do I review my accounting records, such as bank statements, credit card statements, and/or my budget estimates? Do my budgeted projections of expenses and income actually match what I am making and spending or do I need to adjust some things? Which things can/should I adjust?

2. What policies and procedures do I have in place to ensure that I am paid in a timely manner? Am I paid in advance of providing care? What happens if parents are late in paying or bounce a check? Are those consequences in writing? How do I communicate those consequences to parents? Do I have a termination policy in my contract tied to lack of payment from parents?

3. When was the last time I raised my rates/tuition or a fee or considered doing so? When was the last time I added a fee or considered doing so? Am I aware of what the current average rate of payment is for my county? Have I ever calculated my "hourly wage"? If I have, does it feel appropriate to the amount of work I do? Have I ever considered paying myself a monthly/weekly 'salary' from the family child care business income to help keep personal and business finances more separate?

4. How do I ensure I am taking care of my future financial need through my business? How do I plan my retirement contributions so that they aren't overlooked?

1. How often do I review my accounting records, such as bank statements, credit card statements, and/or my budget estimates? Do my budgeted projections of expenses and income actually match what I am making and spending or do I need to adjust some things? Which things can/should I adjust?

2. What policies and procedures do I have in place to ensure that I am paid in a timely manner? Am I paid in advance of providing care? What happens if parents are late in paying or bounce a check? Are those consequences in writing? How do I communicate those consequences to parents? Do I have a termination policy in my contract tied to lack of payment from parents?

3. When was the last time I raised my rates/tuition or a fee or considered doing so? When was the last time I added a fee or considered doing so? Am I aware of what the current average rate of payment is for my county? Have I ever calculated my "hourly wage"? If I have, does it feel appropriate to the amount of work I do? Have I ever considered paying myself a monthly/weekly 'salary' from the family child care business income to help keep personal and business finances more separate?

4. How do I ensure I am taking care of my future financial need through my business? How do I plan my retirement contributions so that they aren't overlooked?

YoungStar Requirements

Under the Business and Professional Practices section of YoungStar, family providers are required to complete a Budget Review for 3, 4, and 5 Stars.

Providers are expected to review their budget annually and make adjustments to future annual budgets as necessary. Providers should not continually update or change dollar amounts on their current budgets, but rather review them periodically and use the information to inform and create future budgets.

The document in this section of the tutorial, "Budget Review" will equip providers in showing at least one area where actual income and expenses from the previous year informed the annual budget for the current year.

At the 3 and 4 Star level, YoungStar requires that providers compare their estimated (budgeted) amounts and actual income and expense amounts spent once a year. This can coincide with the creation of their new annual budget for the next year.

At the 5 Star level, YoungStar requires that providers compare their budget (estimated) amounts and actual income and expense amounts twice a year – at the end of six months and again at the end of the year. This is to ensure that programs at this higher level are creating a fuller picture of their financial situation to be used for planning purposes. Priorities, budget and program planning are intentional and in-line with the program budget; procedures are in place for timely review of budget, and long term fiscal records are maintained and demonstrate sound financial planning.

Providers are expected to review their budget annually and make adjustments to future annual budgets as necessary. Providers should not continually update or change dollar amounts on their current budgets, but rather review them periodically and use the information to inform and create future budgets.

The document in this section of the tutorial, "Budget Review" will equip providers in showing at least one area where actual income and expenses from the previous year informed the annual budget for the current year.

At the 3 and 4 Star level, YoungStar requires that providers compare their estimated (budgeted) amounts and actual income and expense amounts spent once a year. This can coincide with the creation of their new annual budget for the next year.

At the 5 Star level, YoungStar requires that providers compare their budget (estimated) amounts and actual income and expense amounts twice a year – at the end of six months and again at the end of the year. This is to ensure that programs at this higher level are creating a fuller picture of their financial situation to be used for planning purposes. Priorities, budget and program planning are intentional and in-line with the program budget; procedures are in place for timely review of budget, and long term fiscal records are maintained and demonstrate sound financial planning.

Disclaimer: Materials and links provided by WECA on this tutorial do not constitute legal, accounting, tax or finance advice. Participants seeking professional business advice about specific aspects of their program should consult a professional such as a lawyer, accountant, etc.